Insurance is something that most drivers never think about until they have an accident. Car insurance claims are usually a routine request for compensation from an insured individual after they are injured or their car is damaged. Over $170 billion in yearly car insurance claims are made in the United States. There are many factors that come into play when determining where and when to submit a car insurance claim.

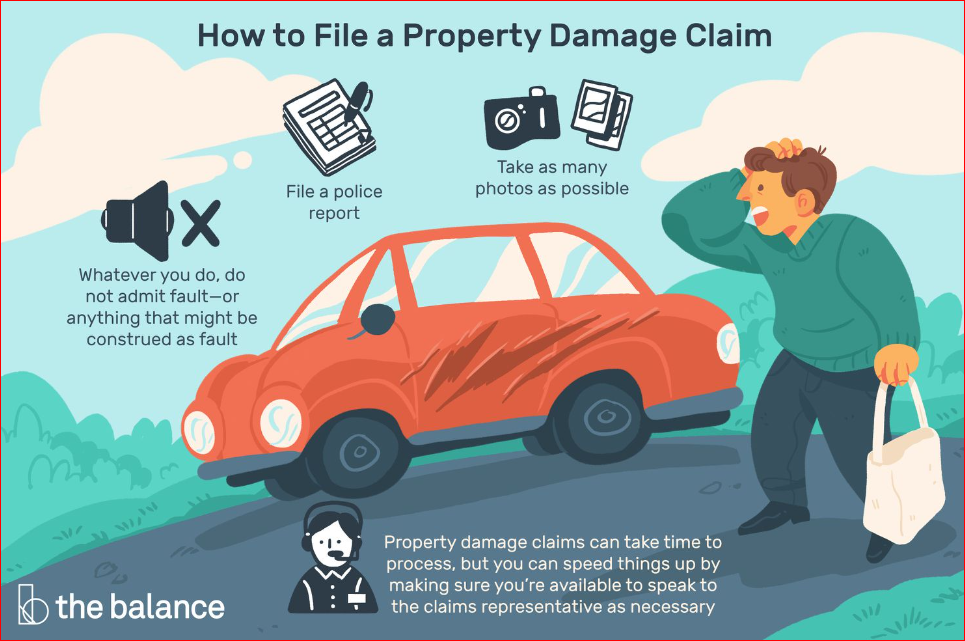

When you get in an accident, whether it is your fault or someone else’s, the first thing you must do is report the claim to the insurance provider. If there is damage to your vehicle, such as dented or damaged parts, immediately remove the damaged items from the vehicle. Write down the details of the damage on the paper so that you can take them with you to the provider’s office to apply for your claim or keep a record of the damage in case it is needed at a later date. In some states, you must submit the accident report to the Insurance Department within a certain amount of time after the accident occurs.

Next, you should contact your insurer to let them know what happened as soon as possible. Most insurance companies have a procedure which requires them to send you a notification of the accident within twenty-four hours after the accident takes place. If you have bodily injury or property damage claims, call the authorities right away to report the incident. It is usually required for police to investigate a claim for bodily injury or property damage, which will lead to further processing of your insurance claim. It is important to report even small accidents to your insurance carrier so that you can work toward getting the best compensation possible.

A claim for injuries or property damage resulting from a fire may require that you submit to a physical exam. You will be asked questions regarding the conditions of the accident site and what caused the fire. When your claim is submitted, it is important that you keep documentation of every statement you make, including supporting documentation such as photographs. If your insurance company determines that your account is valid, they will give you a check for the full amount of your claim. Most insurance companies offer an immediate cash payout for fire claims, but many also offer extended payment plans to help ease the burden of the total loss. In many cases, smoke and water damage claims are processed automatically, but if this is not the case, you should ask the claims adjuster to send you paperwork to process your claim for you.

If you decide to go with your auto insurance carrier to handle your damages, you will need to have a final settlement to show the insurance adjuster. The settlement should be in writing, so that it can be presented in court if necessary. To get a quick and sure payout, take photos of your vehicle, take videos of its repairs, and take detailed notes of how the accident happened and what you did to prevent further damage. As your final claim, include any receipts you may have for the repairs or any photos that may prove you paid for a service or product. This documentation will prove to the insurance company and the court that you were indeed injured in the accident and that you have suffered injuries that require immediate and ongoing medical attention.

When you hire a good public adjuster, he or she will also give you a good settlement, but there are some factors that can make your insurance adjuster less inclined to grant you a settlement. If you do not have much experience dealing with insurance companies, this can be intimidating. However, when you have a professional on your side from the start, things will be much easier. The insurance adjuster has many people who have been through the process before him or her, and they can assist you in the selection of a good settlement. They can also answer any questions that you might have about the process and help you determine if your situation qualifies for one.

Another factor in determining whether or not you will be granted a settlement is your financial situation at the time of the accident. If you were injured because of the negligence of another driver, you will most likely have to file a personal injury lawsuit in order to recover damages. Even if you were not injured in the accident, if you are unable to work because of your injuries, you will have to compensate for lost wages and medical expenses that arise. The best way to recover these costs is to contact an insurance adjuster as soon as possible after the accident so that you can obtain a liability policy or structured settlement from the other driver. The insurance adjuster will look at your records and determine how much the driver actually owed you and what the best pay off amount for your situation would be.

If you are awarded a settlement, you will need to get homeowner’s insurance to cover the amount of your settlement plus a percentage of the actual replacement cost of your home. There are two ways to go about this: you can get a lump sum based on the assessment by the insurance adjuster or you can ask your insurance provider for a monthly payment until you have recovered the full amount of your loss. Your homeowner’s insurance provider may also offer you a structured settlement annuity instead of a lump sum payment if you have older, less expensive items in your house. The insurance provider will pay the full amount of the settlement every month for the duration of the policy.