As a business owner, you know that getting quick business loans for startups can be an important step in your journey to success. Of course, this type of financing can make or break your business. With it, you can move forward with some crucial decisions but also take a big risk. There’s a chance that you’ll need to rely on outside funding sources. But what options do you have if you don’t have access to the traditional bank?

For many companies and entrepreneurs, there are a number of options available to them. Most traditional banks don’t provide small business loan financing. In most cases, they don’t even consider it an option. The main reason is because they don’t consider it a real business loan because it doesn’t involve a mortgage or other traditional means of financing a business venture. That can make a big difference when you’re just starting out – you don’t have a reliable source yet.

Traditional mortgages are loans you obtain through a bank or other lender based on your credit score. Lenders use your credit score to determine whether or not you’re worth putting in the loan. If you have bad credit, you can’t get traditional mortgages, so you may be looking for alternatives such as unsecured loans, which don’t require a mortgage to be qualified. These can be significantly more affordable than traditional loans, so you might want to explore the possibilities.

You can also look at taking out merchant cash advances, as these can be considered a conventional type of small business loan. You can get one without a mortgage by pledging collateral – your business assets, for example. But there’s a catch. These types of business loans usually carry much higher interest rates and other costs than traditional types. This is why it’s often recommended that start-ups should obtain mortgage loans from their existing lenders first.

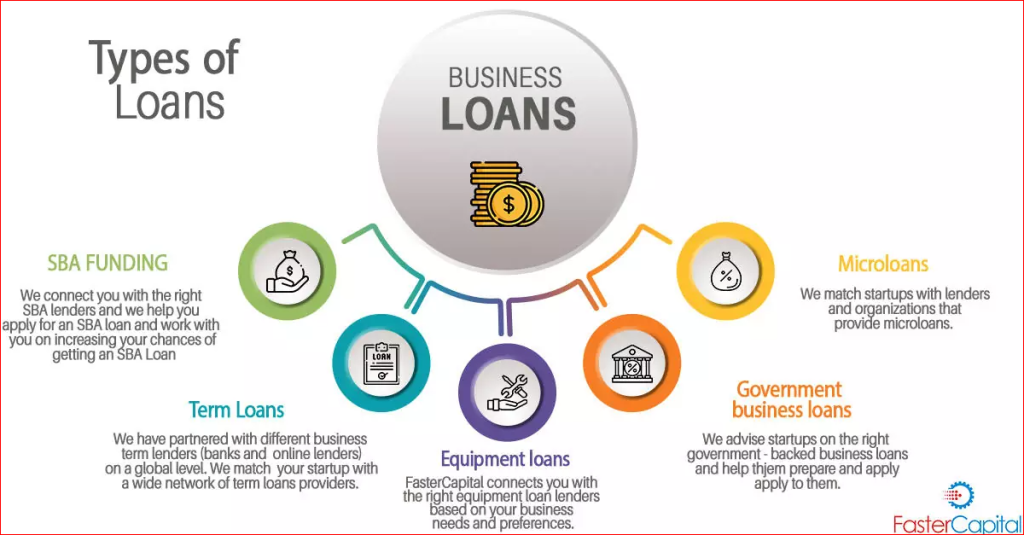

There are other ways to obtain financing besides with a conventional lender. One of the most common is to apply for SBA loans, which are specific lenders’ loans that the federal government provides to qualifying companies. The advantage to this type of financing is that you generally don’t need to provide security for the loan, so there’s no need to worry about the borrower defaulting on the obligation. The downside is that applying for SBA loans can be very time consuming. In addition, interest rates can be higher than conventional mortgage rates.

If you’re looking for a business loan with low interest rates, consider using a non-traditional financial institution, which is another option available to borrowers. For example, there are some monetary institutions that are willing to issue small loans to new businesses – at least for the first two years that the business is open. But these types of lending practices aren’t necessarily conventional.

When it comes to getting quick business loans for startups, it is important to remember the importance of collateral. Because the risk of lending money to an unsecured lender is significantly higher than that of a secured lender, there are several institutions that specialize in providing unsecured business loans. Additionally, there are some lenders who specialize in providing business loans only to small startup companies – which means that they do not do business with larger companies. Because of this feature, if you have the choice, you should find institutions that provide a range of options for collateral types.

In addition to selecting among traditional establishments, you may also want to look into the option of working with an SBA loan provider. Small startup business loans from SBA lenders come with favorable terms, lower interest rates, and faster repayment options. While an SBA loan does have some restrictions related to a specific company, most lenders are able to work with a wide variety of potential borrowers. Because they are generally backed by the federal government, SBA-backed lenders often have less competition and much lower fees and interest rates. If you are interested in securing financing from one of these institutions, your best bet is to speak with a representative from your local office.