Insurance is basically a way of protection against financial loss incurred due to some unforeseen circumstance. It’s a sort of risk management, mostly utilized to mitigate the risk of an unforeseeable or unanticipated loss. Insurance may be for individuals, companies, and public agencies. The main objective of insurance is to compensate for losses that have been incurred due to events that are beyond the control of the insured. Examples of these events are accidents, acts of God, sabotage, human errors, thefts, and disasters.

Insurance is necessary in life, but not so much when it comes to marine perils coverage. Insured persons may not be able to prevent the occurrence of a marine accident, but they can certainly manage to clean it up afterwards. The common consequences resulting from marine accidents are death, injuries, and damage to property. These three things are covered by insurance. However, the policies vary depending on the policyholder, the policy, and the extent of the coverage.

When the insured is the third party, i.e., the third person who suffered the damage, then the victim’s insurance will be paid by the property of the third party, i.e., the insured. This is called ‘direct payment’ or ‘direct liability.’ A shipowner or a cruise liner, as an example, would pay the costs incurred for cleaning and repair of the vessel, minus whatever amount the insurer has paid to the victim. In insurance lingo, direct liability pertains to a claim for which the damages are actually caused by the insured, and not by the third party.

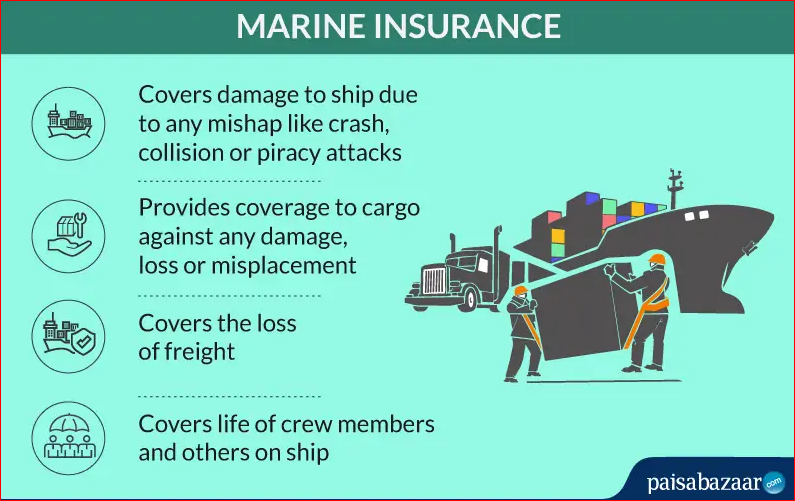

There are two different categories of insurances as stipulated in marine policies: physical and liability insurance. Physical insurance covers incidents such as damage or loss to personal property carried by the insured through negligence or accident. Liability insurance on the other hand protects the insured from claims based on theft, vandalism, or any other acts that may harm his vessels. General insurance, as the name suggests, is the insurance policy that covers financial liabilities caused by the marine environment. While these two insurances have different characteristics, both are important to a ship owner or a cruise liner operator.

The key to determining the right insurance policy is to know the basics of how insurance works. The basic principle of all insurance is that there is risk, there is a reward, and then there is the premium. When shopping around for a policy that caters to your individual needs and preferences, it is important to understand how premium rates vary, and how you can reduce them.

If you want low premiums, you should always go for longer-term disability coverage. When looking for insurance policies, do some comparison shopping to get a better idea of how rates vary between providers. For instance, compare health insurance premiums of different companies by adding the cost of long-term disability coverage. You may be surprised to see that a carrier with a lower premium will be able to offer a similar level of coverage at a higher rate.

In addition, you should choose plans that offer flexibility. The more coverage you require, the higher your premium. It’s better to pay a bit more up front for added protection than to risk having to pay the high cost of a low premium for very little protection. The cheapest premiums often come with hidden costs that increase your premium, so it is important to shop around and learn the difference.

The bottom line: knowing what type of insurance you need, whether it is health insurance, life insurance, marine perils insurance, or any other type, is important for a number of reasons. One, it helps determine the cost of insurance. Two, it helps ensure that your vessel remains seaworthy, even if something happens. And third, knowing the basics about insuring your boat will help minimize any potential losses in case of a disaster.