Life insurance is a legal contract between an insurance company or insurer and an individual, where the insurer promises an individual a specified amount of money on the death of an insured individual, in return for an annual premium paid by the insured. The amount given varies between companies and can even change each year, although it is customary to pay more than usual in yearly terms. Insurance companies use life insurance as a way of protecting their investment, and also as a means to settle the probate estate should the insured die before the maturity of the policy. There are three different types of life insurance: term life, whole life and universal life.

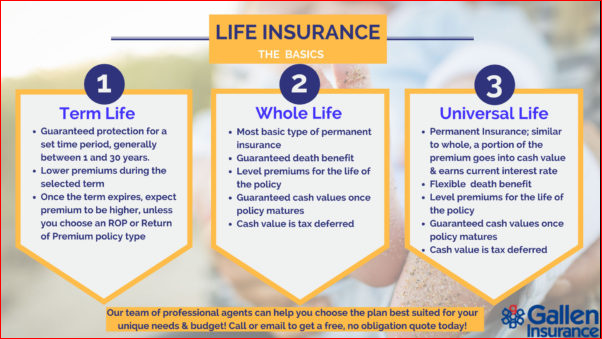

Term life insurance provides coverage for a stated period of time. In this type of policy, the insured pays premiums that increase with the increasing age of the insured, until a payout is made to the policyholder. With this type of policy, the insured may choose from fixed premiums, low premiums, or a combination of both. Depending on the terms of the policy, the insured may choose to invest the cash value of the policy, called a “cash value.” This cash value is not taxable nor is interest from the policy. The policyholder, however, must pay taxes on the cash value if the policyholder outlives the policy, as well as certain fees, during the policy’s lifetime.

Whole life insurance policies are designed to provide coverage for as long as the owner lives. These types of policies are usually less expensive and allow more flexibility, than other types of coverage, such as term coverage. Unlike term policies, these cover dependents after the policyholder dies. A percentage of the policyholder’s annual income is invested to produce cash value, and is then available to the beneficiary, upon death. Beneficiaries receive either a lump sum an award payment, or a monthly income for as long as the policyholder lives.

Variable universal life insurance policies pay a set amount, either daily or in intervals, for a predetermined period of time. The policyholder may borrow against the policy, depending on the contract. Policyholders are allowed to borrow only what is designated as the maximum amount. Policyholders may also choose between a decreasing balance and an increasing balance, which allow them to budget money for future years without decreasing their income.

Monthly premiums are paid by the policyholder and are based on the age of the policyholder. The premium amounts increase over time, with inflation. The cost of a life insurance policy is dependent on many factors, including the age of the policyholder when he or she purchases it, whether or not the policyholder has filed any claims, how much coverage is desired, and the amount of coverage required at the time the policy is purchased. Some factors, such as marital status and occupation, have an effect on premiums.

When purchasing life insurance coverage, young people may want to consider options such as college tuition assistance. They may want to consider the impact of student loans on their family’s future. They may want to consider the value of purchasing a car for their future. Life insurance coverage helps a policyholder’s loved ones in case of death or permanent disability. When purchasing life insurance coverage, policyholders should consider the value of the benefits they will receive, including beneficiaries, college tuition assistance and the ability to pay for healthcare and other bills.

Many people purchase a cash value life insurance policy, also called a Term Life policy, which does not allow investment component. Cash Value pays a death benefit, which may be equal to the surrender value, if invested, up to a certain point. It also allows the policyholder to borrow against the policy’s death benefit. An investor may borrow against the policy’s cash value, according to the insurance company’s policy. Policyholders should consider whether they prefer to have an investment component or not.

Before purchasing life insurance, people are advised to assess their individual and family financial circumstances to determine if it is necessary to have insurance. Policyholders should review their finances to identify their financial hardship. If they have a financial hardship, they may not be able to make a premium payment on a standard policy. In this situation, they can opt for a self-directed health care plan (SDHC) or an appropriate cash value or universal life insurance plan.