Insurance provides protection against risk. In other words, it is a contract between a person and an insurance company that stipulate the insurer’s expected losses in exchange for premium payments. Insurance companies issue insurance policies to provide protection against a number of risks that could befall a business, individual or institution. Insurance companies may issue policies to cover employees against loss or damage sustained while at work, to protect them from loss of income from missed work due to illness or to protect their property from damage by fire or theft. Insurance can also provide a source of retirement income and benefits for workers and their families, as well as help a business meet expenses and obligations that arise from providing jobs.

Many businesses and employers purchase insurance policies on behalf of their employees to provide coverage for a number of potential hazards. In order to determine the premiums to charge for such policies, it is important to assess the risks associated with a business or occupation. For example, if a construction worker were to accidentally fall and break his leg, the employer would need to calculate both the potential financial impact to the business and the level of care needed to cure the leg. These potential financial obligations would then need to be added into the insurance premiums to determine an appropriate premium for that occupation. Similarly, the level of medical attention required would need to be determined.

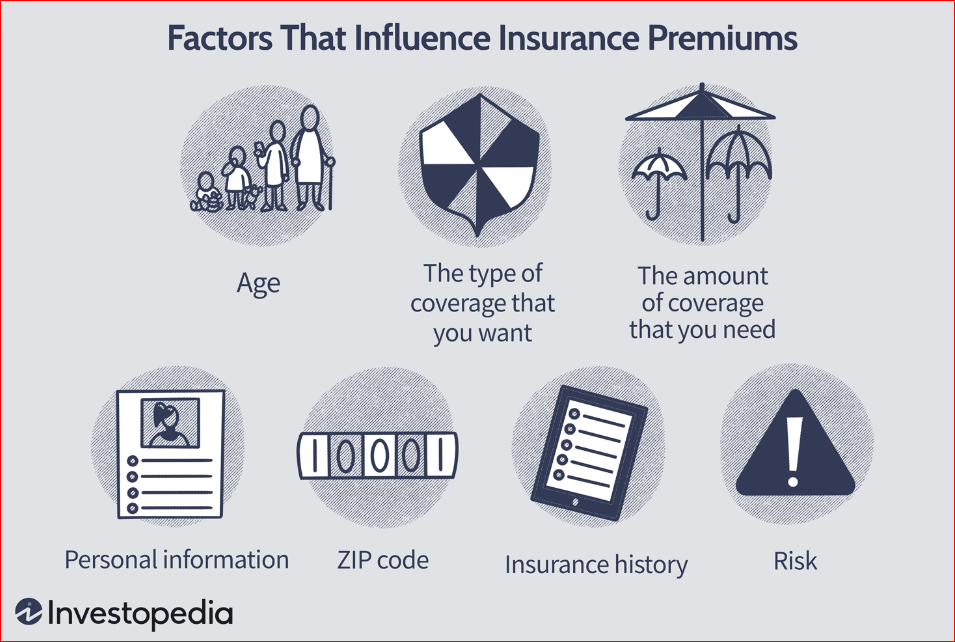

Insurance companies issue insurance policies to provide protection against a number of risks. In general, the rate charged for an individual health insurance policy is based on the sum of expected premiums for each occurrence: the premium for each risk factor is then multiplied by the number of occurrences for which a policy will be purchased. In short, the cost of insurance is expressed as a percentage of the expected losses for each occurrence. Premiums can also be expressed as a ratio of premium amounts to the total number of premium dollars, thus, determining the riskiness of the company in question.

Risk management is crucial to determining premiums and the appropriate levels of risk for different classes of risk. For example, it is a common mistake to assume that the more exposure a business has to a given hazard, the higher its premiums will be. The truth is, businesses expose themselves to more risks than other companies because they are bigger, have more employees and face unique legal risks. Moreover, companies that are highly visible and well-established tend to have the highest premiums because they are perceived as being at a higher risk of experiencing major losses and are therefore “more” likely to default on their insurance policies. In addition, premiums are also determined by risk factors. Examples of risk factors are company stability, industry stability, geographic location, and industry size.

There are several ways to reduce the cost of insurance for your business. One of the easiest and least intrusive methods is to implement cost saving strategies that focus on reducing the level of individual risk. For example, if your company has a large volume of claims or if your company has a high ratio of non-payment claims, your insurance premiums will be higher. If you want to reduce your premiums, it’s important to identify and eliminate risk factors that may lead to excessive claims and/or delinquency. These risk factors include but are not limited to:

To help lower your insurance premiums, it’s important that your company has a solid policy and comprehensive loss response plan in place. Insurance companies rely on your willingness to participate in risk management and take part in the process of claiming and settling claims. When you work with a highly rated insurance company, you’ll receive the same quality service and benefits for your money that you would from a company that charges the lowest premiums, but provides little to no service to its clients. Working with an insurance agent who understands the value of risk management will greatly improve your chances of having your insurance premiums reduced. Similarly, working with an insurance broker who specializes in low premium life and health insurance will enable you to save money on your premiums while still receiving optimal coverage.

Insurance policies such as life insurance are designed to provide you with a source of income when you pass away. Therefore, they carry high premiums. Life insurance policies are typically required as part of a combined life insurance package.

When purchasing life insurance policies, you want to purchase the highest level of coverage that you can legally carry. If you need your policy to cover dependents, then you may want to consider purchasing additional policies that provide coverage for your loved ones upon your death. Purchasing extra policies can often save you money because they do not have as high of a premium as the most basic policies. Conversely, purchasing basic policies allows you to make payment options that are flexible and affordable based on your specific financial circumstances. It’s important to discuss these options with a qualified insurance agent who can guide you in making the right decision for your needs.