Insurance is primarily a way of protection against financial loss from any sort of unexpected or contingent financial loss. It’s a special form of financial risk management, mostly used to mitigate the risk of some future or contingent loss, such as in an insurance policy. In short, we can say that insurance protects us from losses that may occur due to some disaster.

An insurance policy covers you from losses, which may be either actual or implied. Indicative losses are those which are explicitly mentioned in your insurance policy, and implied losses occur on default by the company. A default may be a loss due to federal neglect or a default by the insured party. Examples of implied losses are the regular premiums paid to the insurer by the policyholders.

To protect oneself against unforeseen and unpredictable events, people generally take an insurance policy. But what exactly does insurance provide? The insurance provides two main benefits: financial and non-financial benefits. It serves as a source of income in cases where the insured party becomes unable to earn his or her income. Insurance provides the necessary safety net. For instance, if the insured is injured in an accident and requires expensive medical treatment, then the insurance can provide the funds needed for the medical expenses.

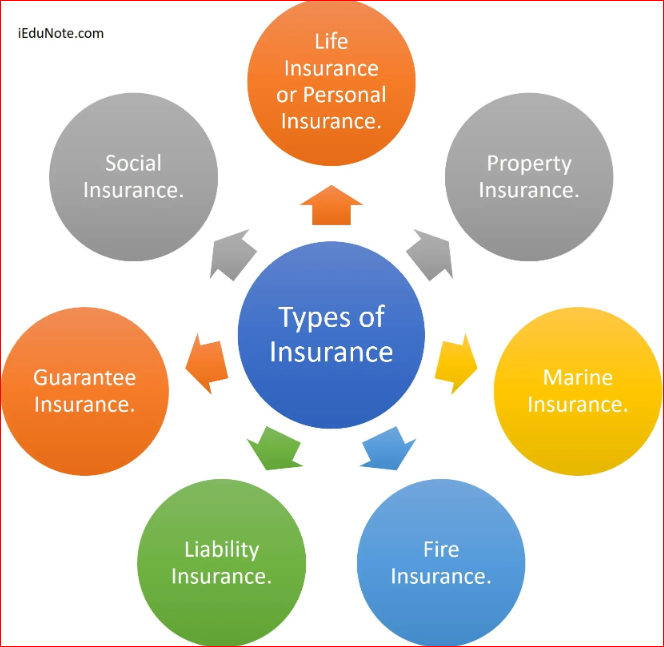

One type of insurance is liability insurance. Liability insurance is designed to compensate for the losses, damages, and legal fees that may result from an accident with an insured party. This coverage could also cover the expenses, losses, and damages incurred in case there is damage to another person’s property while using or operating a vehicle, aircraft, train, boat, or other vehicle. If a driver causes a traffic accident, then liability insurance will pay for the other party’s damages.

What are some common forms of liability insurances? Two major types of liability insurances include bodily injury insurance and marine perils insurance. Bodily injury insurance will cover medical costs and rehabilitation expenses resulting from an insured party’s negligence. Medical expenses and rehabilitation expenses are covered under this type of insurance. Under marine perils insurance, the insurer will pay for damage or loss resulting from any accident caused by a boat, ship, aircraft, or vehicle that is insured by the insurer. Maritime liability insurances come in different packages and offer different coverage.

Another type of insurance coverage is property insurance. Property insurance helps an insurer compensates for the losses or damages suffered due to theft, vandalism, or malicious mischief. Property premiums differ based on the risk of theft, vandalism, or malicious mischief. Property premiums are generally higher than personal premiums.

Home insurance is very important, especially if you live in a high risk area. In fact, having home insurance may affect your car insurance premium. Some insurers will increase the rates of your car insurance because of your location. Insurers consider areas such as high crime, low credit score, and unhealthy and dangerous neighborhood to be high risk areas and will consequently raise your car insurance premium rates.

Although all the three forms of insurance can have similar features and functions, they will not be the same in the sense that they have different features and benefits and the premium for each will differ. The premiums for all the forms of insurance are determined by a number of factors including the age of the insured, the amount of the insured sum, and the insurance coverage chosen. In most cases, the younger the age of the insured, the lower the premium will be. The greater the amount of the insured sum, the higher will be the premium. As you can see, the types of insurances will vary depending on the needs of the insured and the policyholder.