Insurance is a way of protection against financial loss. It’s a crucial form of risk management, mostly used to mitigate against the potential risk of an uncertain or contingent loss in all kinds of businesses. Insurance provides the assurance that things will go well, or else, things go wrong. It can be used to replace lost revenue and payroll, or to mitigate some other risk. In other words, insurance creates an income stream by protecting against losses that might otherwise have been absorbed by the business itself.

In general, there are two types of insurances: General and specific. General insurance policies cover the “whole” body of the insurer. They include such things as property damage, bodily injury, death, and illness. Specific insurance policies pay for specific kinds of risks, such as loss caused by some disaster, theft, or fraud.

A policyholder may decide to renew their current insurance policy by paying a renewal premium. The premium is based on the insurance company’s projected revenue for the upcoming year. When an individual decides to take out another policy, they must pay the renewal premium for the second time around. The first renewal typically costs lower than the second.

An insurance policy is divided into two major sections: “non-collateral” and “collateral”. Collateral is items that will be seized if the insured party has to repay the loan. Non-collateral items, on the other hand, are not valuable enough to be seized. Examples of non-collateral items would be inventory, vehicles, machinery, and personal property.

One kind of specialized type of insurance policy is the travel insurance policy. There are several types of travel insurance policy. For example, if an individual travels overseas for a special event that must be booked, the policy may specify that certain medical bills must be paid. This is a good policy if the person traveling knows they will have to meet with unforeseen medical expenses during the trip.

A health insurance policy is one that insures against medical or other expenditures above a preset limit. This limit is usually set by the insurance company and may be different for different types of policies. Policy holders are required to pay a premium in order to obtain coverage. The premium is determined by a combination of several factors, such as age, gender, coverage needs, and the health history of the policy holder. These factors are also influenced by the insurer.

There are two basic types of auto insurance: group and individual. Group premiums are more affordable than individual premiums, and the insurer will offer discounts to policyholders who are part of a large group. Individual premiums are more expensive and the insurer will give discount to new policy holders who have never had any insurance history. Many companies also offer different kinds of discounts to policy holders.

Insurance can help save you money and protect you from unforeseen events. In the case of health insurance, coverage can also protect the policy holder from financial hardship due to an unexpected illness or injury. Insurance can also prevent loss of work productivity and possible foreclosure of the home or apartment due to medical or disability reasons. Long-term disability coverage can also protect the lender from future loss of income and might allow you to refinance your mortgage when needed. It’s always advisable to compare free insurance quotes online so you can find the best coverage and premiums to meet your individual needs at the lowest cost.

You may want to consider life insurance in the event that you pass away unexpectedly. Term life can be purchased for a specific length, term life policies don’t have any renewable options, so it is very important to read the terms and conditions carefully before purchasing a term life policy. Some life insurance plans offer dividends or bonuses upon purchase, while others may want you to take out a loan prior to signing up. Another kind of insurance policy is universal life coverage that pays a cash benefit to the beneficiary upon death or cancellation of the policy. This type of coverage has a tax cost so you may want to check with your accountant to see if it is a good investment. Most universal policies last up to 30 years.

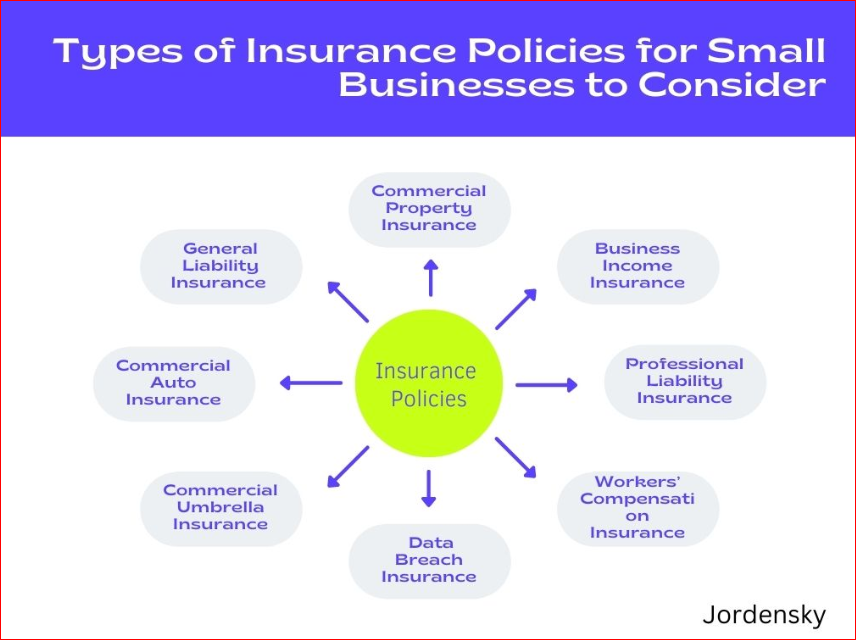

Business insurance helps protect your company from liability, litigation, and loss. It can be purchased to protect you against property damage, loss, and employee injury claims. Different types of business insurance help protect different parts of your business depending on its use. For example, property insurance protects the physical building and contents of your business. Liability insurance helps protect you from lawsuits associated with your business. Many people own their own small business and have liability insurance, but it’s also important to remember that small business insurance is just that, a small portion of your overall insurance protection.

Workers’ compensation is very important for employers that employ individuals. Workers’ compensation helps to pay medical expenses, lost wages, pain and suffering, and other expenses that result from an on the job accident. Many employees consider a workers compensation policy important, because not only can they receive the assistance they need when injured on the job, but if they are injured on the job and seek damages, the employer may be responsible for those expenses.